Across agricultural regions in North America and beyond, buyers and especially individuals outside farming industries are often surprised by the persistent strength of used tractor prices. Even machines with thousands of operating hours can command values that seem disproportionate to their age. This phenomenon is not confined to one country or farming system, but reflects broader global forces shaping modern agriculture. The high cost of used tractors is the result of interconnected economic, technological, and structural factors that extend well beyond simple depreciation.

Rising New Tractor Prices Push Demand Towards the Used Market

One of the most influential drivers of used tractor prices worldwide is the escalating cost of new machinery. In the United States, Europe, and other major agricultural exporters, manufacturers have steadily increased prices as tractors become more technologically advanced, not unlike modern automobiles. Precision agriculture systems, emissions-compliant engines, digital controls, and sophisticated hydraulics have become standard rather than optional.

READ: The Long Rise of California’s Almond Industry

While these features improve efficiency, fuel economy and data-driven decision-making, they also significantly raise production costs. For example, today some high-end John Deere and Fendt models designed for large scale operations can cost $500,000 or more. In 1958, the price of a brand-new Oliver Super 44 cost $2,200. However, regardless of era, tractors have always been a major capital investment relative to median household income. For many farmers, particularly small and mid-sized operators, the price of a new tractor has moved beyond practical reach. As a result, demand flows directly into the used market, increasing competition for second-hand machines, and sustaining higher prices across borders.

Global Supply and Demand Imbalances

Used tractor markets operate within a global supply-and-demand framework shaped by the long working life of agricultural machinery. Tractors are durable capital assets designed to remain productive for decades, resulting in slow replacement cycles across virtually all farming regions. In the U.S. Midwest, Western Europe and parts of South America, farmers frequently extend equipment use due to high replacement costs, volatile commodity prices, and tighter financing conditions. Similar behaviour is evident elsewhere, although driven by different constraints, such as limited access to credit, smaller farm incomes or reliance on shared ownership models.

At the same time, demand for mechanized farming continues to expand worldwide. Developing agricultural regions across Africa, Asia, and Eastern Europe increasingly seek reliable used tractors imported from North America, and Europe as cost-effective alternatives to new machinery. This growing international demand reduces local availability in exporting markets and exerts sustained upward pressure on prices, particularly for proven models capable of operating across diverse climates, soil types, and regulatory environments.

Older Tractors and Perceived Build Quality

A recurring theme across global markets is the belief that older tractors were built to a higher mechanical standard. Many machines produced in the mid-to-late twentieth century relied more heavily on steel construction, mechanical drivetrains, and simpler engineering. These characteristics are often associated with longevity, durability, and easier maintenance.

In contrast, modern tractors rely heavily on electronics and proprietary software. While technologically impressive, these systems can be expensive to diagnose and repair without dealer access. For buyers in rural U.S. regions, remote parts of Australia or developing markets with limited dealer networks, older tractors represent dependable tools rather than technological liabilities. This perception reinforces their value and helps explain why depreciation slows dramatically once a tractor proves its durability.

Replacement Parts Availability and Cost

Replacement parts play a crucial role in sustaining used tractor prices. Manufacturers with long production histories and large installed fleets tend to maintain support for legacy models over extended periods, ensuring parts remain widely available through authorized dealer networks, and established aftermarket suppliers. When parts supply is reliable, buyers are more willing to invest in older equipment, reinforcing confidence, and supporting higher resale values. A widely cited example is the John Deere 4020, introduced in 1964, which remains one of the most comprehensively supported tractors ever produced. Essential components such as clutches, hydraulic pumps, fuel system parts, cooling components and steering assemblies continue to be manufactured as current-production items rather than relying solely on remaining inventory or salvage sources.

READ: Saudi Arabia, the Desert Kingdom that Decided to Feed Itself

Similar long-term parts availability is evident for other legacy models, including Massey Ferguson tractors, such as the MF 135 and MF 165, Ford and New Holland models from the 3000 and 5000 series respectively, and selected International Harvester tractors from the late 1960s, and 1970s. This depth of support allows machines from this era to remain economically viable many decades after manufacture and plays a direct role in sustaining their strong market values.

Conversely, constraints affecting the supply of certain components can push used prices higher still. Shortages of hydraulic assemblies, specialized transmission parts, and electronic modules, particularly for newer machines, have raised maintenance costs in recent years. In the United States and Europe, delays in sourcing parts for modern tractors have led many operators to retain older, mechanically simpler machines for longer periods, reducing trade-ins, and tightening supply in the used market. In some instances, complete tractors are purchased specifically for dismantling and parts recovery, further reducing the number of intact machines available for resale, and amplifying scarcity-driven pricing effects.

Supply Chain Disruptions and Manufacturing Delays

Global supply chain disruptions have had lasting effects on agricultural equipment markets. Events such as the COVID-19 pandemic, geopolitical conflicts, semiconductor shortages, and shipping bottlenecks delayed new tractor production across continents. Manufacturers in North America and Europe experienced order backlogs extending well beyond typical delivery timelines.

When new tractors became harder to source, many farmers turned to the used market out of necessity rather than preference. This shift in demand was visible in both U.S. and international markets, where auction results for pre-owned tractors climbed sharply and have not yet fully normalized. For instance, an auction in Munroe City, Indiana, a 2007 John Deere 9620 with under 2,000 hours sold for $185,250, setting a high-water mark for its model. Late 2024 auctions similarly saw elevated prices, including a 2014 Challenger MT865C with approximately 1,450 hours, fetching $341,000, exceeding prior sales for that model.

Looking at broader trends, a review of high-horsepower tractors (300+ hp) sold at auction between 2020 and 2022 revealed consistent double-digit price gains, with some models increasing by nearly 40 percent during this period. These figures highlight the combined effects of constrained new equipment supply and competitive bidding, which together have driven used tractor values upward, and maintained pressure on prices across markets.

These disruptions also impacted spare parts supply, reinforcing incentives to maintain existing machinery rather than replace it.

Strong Secondary Markets and Auction Culture

In countries such as the United States, Canada and Australia, agricultural auctions play a significant role in price discovery. Online and live auctions expose used tractors to national and international buyers simultaneously, often driving prices higher than private sales would achieve.

READ: How Much of Canada Is Actually Farmland?

Export buyers frequently participate in these auctions, particularly for proven tractor models with global compatibility. When overseas demand enters domestic auctions, prices adjust upward to reflect global willingness to pay. This dynamic means that even local buyers are indirectly competing with international markets, reinforcing sustained price levels.

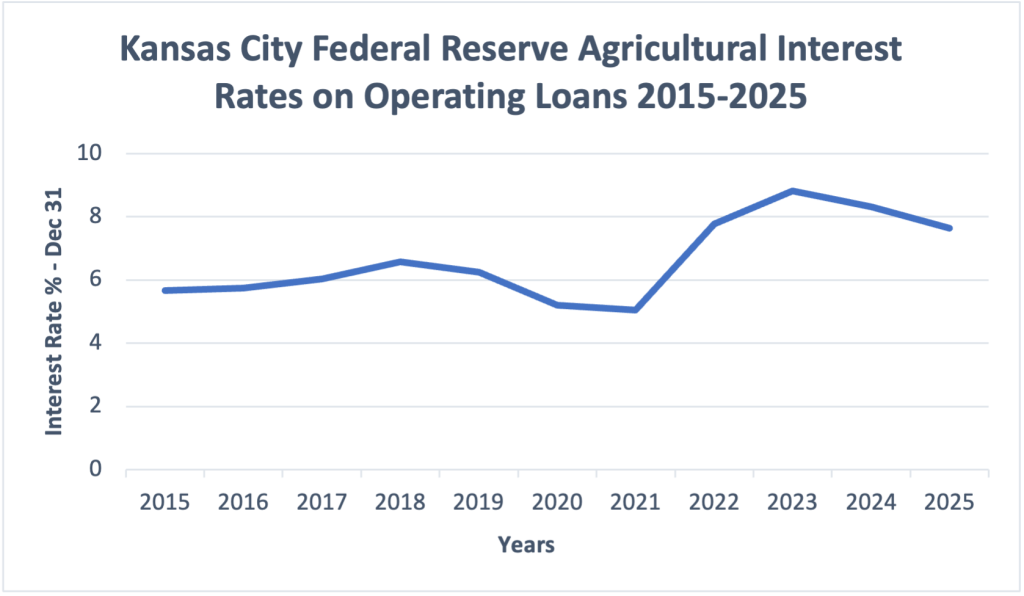

Financing Conditions and Capital Preservation

Macroeconomic conditions also influence used tractor pricing. Rising interest rates globally have increased borrowing costs for large equipment purchases. New tractors typically require financing, making them more sensitive to changes in credit conditions.

Used tractors, particularly those purchased outright or with short-term financing, become relatively more attractive during periods of tighter credit. In both U.S. and international contexts, farmers prioritize capital preservation, opting for used machinery that offers predictable performance without long-term debt obligations. This behaviour increases demand and supports higher prices.

Financing options for agricultural equipment generally fall into two categories: commercial loans from private banks and credit unions, and government-backed loans, such as those offered by the USDA Farm Service Agency (FSA). Commercial loans reflect prevailing market interest rates and are typically used by larger or well-established farms, while FSA loans provide lower-cost options aimed at smaller or beginning farmers.

The divergence between these two types of financing means that changes in either can influence purchasing behaviour. When commercial rates rise, many operators turn to FSA loans if eligible, or defer new equipment purchases entirely in favour of the used market. This dynamic reinforces the resilience of used tractor demand, as farmers weigh the trade-off between financing cost, and machinery reliability.

Environmental Regulations and Compliance Costs

Environmental regulations continue to reshape tractor manufacturing globally. Emissions standards such as Tier 4 Final in North America and Stage V in the European Union require advanced exhaust treatment systems that raise production complexity and cost. These regulatory pressures increase new tractor prices and, by comparison, enhance the appeal of older machines.

In some regions, older tractors remain legally operable without costly emissions upgrades, making them financially preferable despite lower fuel efficiency. This regulatory asymmetry helps preserve used tractor demand across different jurisdictions.

Technological Sufficiency Rather Than Obsolescence

Unlike consumer electronics, tractors do not become functionally obsolete at the same pace as technology advances. While GPS guidance, automation and data integration offer measurable benefits, they are not essential for all farming operations. Many core agricultural tasks remain effectively performed by tractors that were built decades ago.

As a result, technological progress enhances new machinery without necessarily diminishing the utility of older equipment. This technological sufficiency explains why used tractors maintain relevance and value well beyond conventional depreciation timelines.

A Globally Reinforced Pricing Structure

The continued high cost of used tractors is not driven by a single factor, but by a convergence of global influences. Rising new equipment prices, constrained supply, durable build quality, parts availability, regulatory pressures, and international demand all contribute to a resilient used market. From the American Midwest to European arable farms, and export-oriented markets worldwide, used tractors remain expensive because they continue to meet real operational needs under evolving economic conditions.

Understanding these dynamics helps explain why used tractors are not merely cheaper alternatives, but strategic investments shaped by global agricultural realities.

Do you swear by an older tractor that’s still going strong, or have you made the jump to modern technology — and was it worth it?

Sources

- December 2022 used equipment market review. (2023, January 19). Tractor Zoom. Retrieved March 12, 2026, from https://www.tractorzoompro.com/our-solutions/equipment-market-trends/december-2022-used-equipment-market-review

- Easterlund, P. (2022, June 29). TractorData.com Oliver Super 44 tractor information. Retrieved March 12, 2026, from https://www.tractordata.com/farm-tractors/000/6/6/665-oliver-super-44.html

- Federal Reserve Bank of Kansas City. (2026, February 16). Kansas City Fed Agricultural interest rates on operating loans. YCharts. Retrieved March 12, 2026, from https://ycharts.com/indicators/kansas_city_fed_agricultural_interest_rates_on_operating_loans

- Grassi, M. J. (2025, February 27). A Perfect Storm Is Driving Up New and Used Tractor Prices. AgWeb Farm Journal. Retrieved March 12, 2026, from https://www.agweb.com/news/machinery/perfect-storm-driving-new-and-used-tractor-prices

- Peterson, G. (2025, January 8). December 2024: A Month to Remember. AgWeb Farm Journal. Retrieved March 12, 2026, from https://www.agweb.com/news/machinery/used-machinery/december-2024-month-remember